Budget Report 2020: Capital Taxes

Capital gains tax (CGT) rates

The current rates of CGT are 10%, to the extent that any income tax basic rate band is available, and 20% thereafter. Higher rates of 18% and 28% apply for certain gains; mainly chargeable gains on residential properties with the exception of any element that qualifies for Private Residence Relief.

There are two specific types of disposal which potentially qualify for a 10% rate up to a lifetime limit for each individual:

- Entrepreneurs’ Relief (ER). This is targeted at directors and employees of companies who own at least 5% of the ordinary share capital in the company, provided other minimum criteria are also met, and the owners of unincorporated businesses.

- Investors’ Relief. The main beneficiaries of this relief are external investors in unquoted trading companies who have newly-subscribed shares.

Investors’ Relief has a lifetime limit of £10 million, however the lifetime limit position for ER has been changed in the Budget and is considered further below.

CGT annual exemption

The CGT annual exemption is £12,000 for 2019/20 and £12,300 for 2020/21.

Entrepreneurs’ Relief (ER)

The lifetime limit is reduced from £10 million to £1 million for ER qualifying disposals made on or after 11 March 2020.

There are special provisions for disposals entered into before 11 March 2020 that have not been completed.

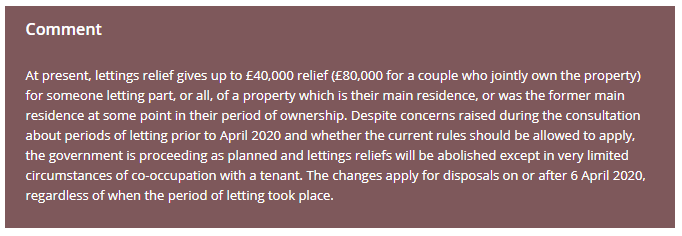

Private Residence Relief (PRR)

Draft legislation has been issued to make changes to the PRR regime from 6 April 2020. For properties that have not been occupied throughout the period of ownership, available deductions for capital gains tax purposes will be amended as follows:

- the final period exemption will be reduced from 18 months to nine months (there are no changes to the 36 months that are available to disabled persons or those in a care home)

- lettings relief will be reformed so that it only applies in those circumstances where the owner of the property is in shared occupancy with a tenant.

Payments on account and 30 day returns

Legislation has been enacted to change reporting obligations for residential property gains chargeable on UK resident individuals, trustees and personal representatives. Also introduced is a requirement to make a payment on account of the associated CGT liability. For disposals made on or after 6 April 2020:

- a tax return is required if there is a disposal of UK land on which a residential property gain accrues

- CGT is required to be computed on the reported gain in the tax return.

The return needs to be filed and the CGT paid within 30 days of the completion date of the property disposal.

The new requirements do not apply if a chargeable gain does not arise, for example where the gains are covered by PRR.

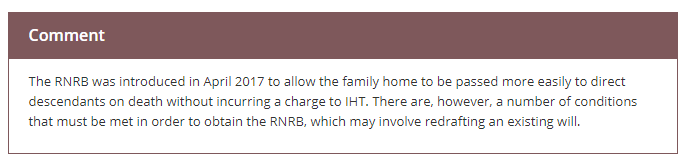

Inheritance tax (IHT) nil rate bands

The nil rate band has remained at £325,000 since April 2009 and is set to remain frozen at this amount until April 2021. An additional nil rate band, called the ‘residence nil rate band’ (RNRB), continues to be phased in. For deaths in 2019/20 it is £150,000 rising to £175,000 for deaths in 2020/21. Thereafter it will rise in line with CPI.

Stamp Duty Land Tax (SDLT) surcharge

A SDLT surcharge on non-UK residents purchasing residential property in England and Northern Ireland is to go ahead. The 2% surcharge is to take effect from 1 April 2021. Where contracts are exchanged before 11 March 2020 but complete or are substantially performed after 1 April 2021, transitional rules may apply.

Please see the pages below for more information

Income Tax and Personal Savings

Tags.budget, budget 2020